Daily

Treasury Bills vs CDs: Which Pays More Right Now?

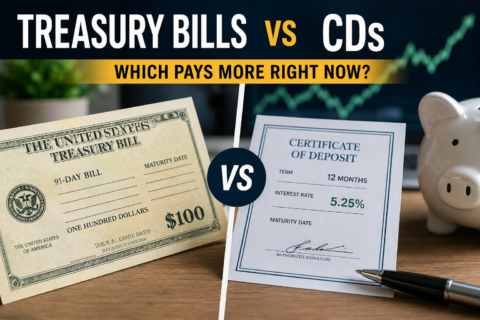

Understanding Treasury Bill and CD Rates Comparing safer ways to grow cash. Photo by AI....

May 31, 2026

Understanding Treasury Bill and CD Rates Comparing safer ways to grow cash. Photo by AI....

May 31, 2026

What Most Employees Miss Every fall, millions of Americans open...

Smart Tax Refund Planning Before the Money Hits Most Americans...

How Expense Ratios Work Inside Investment Funds Most investors spend...